wreath how to

http://blog.cb2.com/2009/10/14/wreath-how-to/

Sorry for the posting delay! It's been an exhausting week and I'm scrambling to get everything done. But check back later today and I'll have a post up!

More free coffee!

Dunkin Donuts is offering free samples of coffee here. I didn't want to wait until Friday to post it, since the last freebie I posted ran out of supplies really quickly. Click "free sample" at the top of the page and enter your information!

Thanks to Devon for the link!

Thanks to Devon for the link!

Monday Money Saver #6: Five Easy Ways to Increase Income

The best way to have more money in the future, is to find ways to increase your income. $5 here or there may seem small, but it adds up over time. Here are a few ways you can earn extra income - either to save, or to use as your spending money, depending how you want to plan your finances.

1. Interest

Switch from a regular savings account to a high interest savings account. I switched around this time last year, and went from earning $0.25/year in interest, to what will be nearly $30 by the year's end. Wednesday's post will cover several good websites for getting a higher yield on your money. Many of these sites are FDIC insured, which means you will not have to worry about losing your money. You may potentially make more interest in a Money Market account, but it will also be riskier, since it is not insured by the government.

2. Surveys

When I was younger, my mom was constantly visiting the little survey place in the mall. I was bored out of my mind waiting for her as a kid, but now that I'm in a good 'target demographic', I can totally see why she did it. Earning anywhere from $5 to $20 for a little bit of your time, you've paid for your lattes for the week, and can divert what you would normally spend into savings or investments. You can also participate in online surveys that pay, although these are harder to come by.

3. Blogging

I started this blog because I wanted to get my money-saving ideas written down, so I can hold myself accountable to what I know are smart ideas. It's too easy to get lazy when you aren't thinking about frugality all the time. But since I was starting a blog anyway, it was incredibly easy to add in a Google Adsense bar. I may not earn much (people who blog for a living can make much more, because they have the time to put in to it). But $5 here or there really adds up over time.

4. Craigslist or Ebay

That's right. Last week's website was Craigslist, and the post focused on how to save money on buying things for your home. But you can use it to make money too! Every once in a while, go around your home and collect things that you don't need or don't use. Then take a few minutes and post it on Craiglist or Ebay, and wait for someone to want to buy your things! Not only did you make a few bucks, but you also cleared a little clutter.

5. Part-time Job

Ok. Admittedly, this one is a little more difficult. Some people don't have the time or the energy. But there are tons of jobs that are flexible and do not require steady committment. Find what you love to do, and see if you can fit it into your schedule. If you love kids but don't have your own, babysit for a friend's children or put an ad on Craigslist. If you like interacting with people, pick up a couple evening or weekend shifts at a restaurant. If you are a night owl like my fiance, take a Friday or Saturday night and drive a taxi. You can easily make $100 for one night of working at a restaurant or babysitting, or $200 for a 12 hour cab shift.

The only thing holding you back from making money is you! Adapt any of these ideas to fit your own life, and then you'll have a lot more money at the end of a year than you would have expected!

1. Interest

Switch from a regular savings account to a high interest savings account. I switched around this time last year, and went from earning $0.25/year in interest, to what will be nearly $30 by the year's end. Wednesday's post will cover several good websites for getting a higher yield on your money. Many of these sites are FDIC insured, which means you will not have to worry about losing your money. You may potentially make more interest in a Money Market account, but it will also be riskier, since it is not insured by the government.

2. Surveys

When I was younger, my mom was constantly visiting the little survey place in the mall. I was bored out of my mind waiting for her as a kid, but now that I'm in a good 'target demographic', I can totally see why she did it. Earning anywhere from $5 to $20 for a little bit of your time, you've paid for your lattes for the week, and can divert what you would normally spend into savings or investments. You can also participate in online surveys that pay, although these are harder to come by.

3. Blogging

I started this blog because I wanted to get my money-saving ideas written down, so I can hold myself accountable to what I know are smart ideas. It's too easy to get lazy when you aren't thinking about frugality all the time. But since I was starting a blog anyway, it was incredibly easy to add in a Google Adsense bar. I may not earn much (people who blog for a living can make much more, because they have the time to put in to it). But $5 here or there really adds up over time.

4. Craigslist or Ebay

That's right. Last week's website was Craigslist, and the post focused on how to save money on buying things for your home. But you can use it to make money too! Every once in a while, go around your home and collect things that you don't need or don't use. Then take a few minutes and post it on Craiglist or Ebay, and wait for someone to want to buy your things! Not only did you make a few bucks, but you also cleared a little clutter.

5. Part-time Job

Ok. Admittedly, this one is a little more difficult. Some people don't have the time or the energy. But there are tons of jobs that are flexible and do not require steady committment. Find what you love to do, and see if you can fit it into your schedule. If you love kids but don't have your own, babysit for a friend's children or put an ad on Craigslist. If you like interacting with people, pick up a couple evening or weekend shifts at a restaurant. If you are a night owl like my fiance, take a Friday or Saturday night and drive a taxi. You can easily make $100 for one night of working at a restaurant or babysitting, or $200 for a 12 hour cab shift.

The only thing holding you back from making money is you! Adapt any of these ideas to fit your own life, and then you'll have a lot more money at the end of a year than you would have expected!

Do This Before You Get Married!

One of the biggest causes of arguments, stress, and unhappiness in a marriage is money. Everyone knows someone who has argued with their spouse (or former spouse!) about money, and generally it isn't pretty. Whether it devolves into name calling, insults, or storming out, money fights are nasty business. So don't sabotage your marriage before you are even married! This post will cover some questions that you absolutely need to ask before you get married, as well as tips about what to avoid in financial discussions.

My fiance and I went to a marriage prep class last weekend, which is required by the Catholic Church before getting married. Although the class lasted two days and covered a wide range of topics, the one that made everyone chuckle/groan was the topic of finances.

Generally, people fall into one of three categories: Savers, Spenders, or a little of both. When Savers and Spenders get married, it can lead to some pretty intense 'discussions' about where money goes. If you don't handle these discussions the right way, or you can't find a way to reconcile your opinions, you're in for a rocky ride. If you can create a set of common priorities, though, you will be able to weather many storms.

For example, my mom is definitely a spender, whereas my dad is a saver. They have had their fair share of disputes over money, but they are still together after 25 years and two kids. The key to this is that they both had the same priorities - my brother and me. It was critical to them that we both received a good education and the opportunities to pursue our interests, without turning into spoiled brats. If they had to go without the fancy TV so that we could do Scouting or sports without going into debt, they did it.

They were also able to compromise. My mom would love to spend tons of money on nice clothes and a big house, whereas my dad would rather save for retirement and wear his clothes until they fell apart. They ended up reaching a middle ground, with a modest spending and plenty of savings. Sure, they still disagree sometimes, but that's normal when people have different opinions. The important thing is how they handle it.

Talking to your future spouse is critical, so that you are both on the same page once you get married. Here is a list of questions that you should answer before getting married, and a list of things to NEVER EVER EVER do when discussing money together.

QUESTIONS

1. Are you a Saver or a Spender, or somewhere in between? How will that affect your budget? (and you MUST have a budget!)

2. What are your financial priorities? (owning a home, children's education, travel, retirement savings, etc) Another critical factor to discuss here is whether your priorities are things or experiences. If you both like things, it might make more sense to get that flat screen TV. But if you like experiences, you might choose to spend the money on a weekend getaway or date nights.

3. Is the money you earn 'yours' or 'ours'? Will you keep separate bank accounts, combine them into one, or have a some of each?

4. Who will be in charge of paying the bills? Will you take turns, work as a team, or will one person take responsibility?

5. Do you have a will or trust account set up? If something happens to one of you, what happens to the assets and debt of the other person? Who is the beneficiary on life insurance policies, retirement plans, or other financial accounts? This is a slightly morbid, but necessary step in combining your lives. Planning for the death of a spouse might seem depressing at first, but God forbid it ever happens, the lack of stress on financial matters will be much appreciated.

NEVER EVER DO THESE THINGS

1. Do not discuss money if either of you are H.A.L.T. (Hungry, Angry, Lonely, Tired) This will only lead to crankiness and problems. Of course if it is an emergency, that's one thing. But if someone just had a hard day at work and needs to decompress, or is ravenously hungry, it might not be the best time to discuss the budget.

2. Never, ever call each other names, insults, or anything derogatory. This will only cause hurt feelings, and won't solve anything. You might feel like you've won temporarily, but in the long run you'll be hurting both of you. You should have left name-calling back in grade school - don't bring it into your marriage. Nobody is dumb, stupid, or anything like that. If you truly think so, you shouldn't be getting married!

3. Do not leave your spouse out of financial decisions. Even if you have agreed that one of you will be responsible for paying bills and handling the finances, make sure that both of your priorities are represented, and that you both know your financial situation. If you choose to be a one income household to raise children, the person without a career should not feel trapped. Do not play mind games with money. It's important for both of you to know your financial situation in case anything happens to the main bill-payer. If he or she becomes incapacitated, bills still need to be paid.

My fiance and I went to a marriage prep class last weekend, which is required by the Catholic Church before getting married. Although the class lasted two days and covered a wide range of topics, the one that made everyone chuckle/groan was the topic of finances.

Generally, people fall into one of three categories: Savers, Spenders, or a little of both. When Savers and Spenders get married, it can lead to some pretty intense 'discussions' about where money goes. If you don't handle these discussions the right way, or you can't find a way to reconcile your opinions, you're in for a rocky ride. If you can create a set of common priorities, though, you will be able to weather many storms.

For example, my mom is definitely a spender, whereas my dad is a saver. They have had their fair share of disputes over money, but they are still together after 25 years and two kids. The key to this is that they both had the same priorities - my brother and me. It was critical to them that we both received a good education and the opportunities to pursue our interests, without turning into spoiled brats. If they had to go without the fancy TV so that we could do Scouting or sports without going into debt, they did it.

They were also able to compromise. My mom would love to spend tons of money on nice clothes and a big house, whereas my dad would rather save for retirement and wear his clothes until they fell apart. They ended up reaching a middle ground, with a modest spending and plenty of savings. Sure, they still disagree sometimes, but that's normal when people have different opinions. The important thing is how they handle it.

Talking to your future spouse is critical, so that you are both on the same page once you get married. Here is a list of questions that you should answer before getting married, and a list of things to NEVER EVER EVER do when discussing money together.

QUESTIONS

1. Are you a Saver or a Spender, or somewhere in between? How will that affect your budget? (and you MUST have a budget!)

2. What are your financial priorities? (owning a home, children's education, travel, retirement savings, etc) Another critical factor to discuss here is whether your priorities are things or experiences. If you both like things, it might make more sense to get that flat screen TV. But if you like experiences, you might choose to spend the money on a weekend getaway or date nights.

3. Is the money you earn 'yours' or 'ours'? Will you keep separate bank accounts, combine them into one, or have a some of each?

4. Who will be in charge of paying the bills? Will you take turns, work as a team, or will one person take responsibility?

5. Do you have a will or trust account set up? If something happens to one of you, what happens to the assets and debt of the other person? Who is the beneficiary on life insurance policies, retirement plans, or other financial accounts? This is a slightly morbid, but necessary step in combining your lives. Planning for the death of a spouse might seem depressing at first, but God forbid it ever happens, the lack of stress on financial matters will be much appreciated.

NEVER EVER DO THESE THINGS

1. Do not discuss money if either of you are H.A.L.T. (Hungry, Angry, Lonely, Tired) This will only lead to crankiness and problems. Of course if it is an emergency, that's one thing. But if someone just had a hard day at work and needs to decompress, or is ravenously hungry, it might not be the best time to discuss the budget.

2. Never, ever call each other names, insults, or anything derogatory. This will only cause hurt feelings, and won't solve anything. You might feel like you've won temporarily, but in the long run you'll be hurting both of you. You should have left name-calling back in grade school - don't bring it into your marriage. Nobody is dumb, stupid, or anything like that. If you truly think so, you shouldn't be getting married!

3. Do not leave your spouse out of financial decisions. Even if you have agreed that one of you will be responsible for paying bills and handling the finances, make sure that both of your priorities are represented, and that you both know your financial situation. If you choose to be a one income household to raise children, the person without a career should not feel trapped. Do not play mind games with money. It's important for both of you to know your financial situation in case anything happens to the main bill-payer. If he or she becomes incapacitated, bills still need to be paid.

Wednesday Website #5: Craigslist.org

This post might be obvious to some, but it definitely is worth mentioning.When it came time to furnish our apartment, we immediately went to Craigslist.org. You can find excellent pieces of furniture for very little money, if you can figure out when the most items will hit the market in your locale. For example, if you live in a city with a large university, check Craigslist frequently between the months of May and September and you'll be rewarded with people moving out, people moving in, and lots of furniture being posted.

We live in a large city, which helps provide a steady flow of Craigslist items. If you know what you are looking for, and you check frequently, you can score awesome deals. The picture above is our living room, and all of the furniture is from Craigslist or IKEA.

Here's the breakdown:

Couch - $150

Price included delivery and help getting it into the apartment. This couch is a clean dark grey material, and is as big as a twin bed if you remove the back cushions. It's great for guests to stay on, or for taking a nap (trust me - it's ridiculously comfortable and makes you never want to get up!).

Chairs - $50 each

I had been eying these cream colored TULLSTA chairs from IKEA for months. I didn't want to pay the $99 price the store asks for brand new chairs, so I kept an eye out on Craigslist. It took several months, during which I saw it in red, black, or a single cream chair, but eventually I found someone selling several of these. I snapped them up instantly! There is only a couple small smudges on the material, but they are barely noticeable. I can either try steam cleaning them, or just get a washable slipcover.

Bookcase - $40 for two

We had been in need of bookcases for about a year. Our books were sitting in white plastic milk crates since we moved here, and they were in need of a new home. I kept an eye out for nice wooden bookcases, and was rewarded with these foldable bookcases. They happen to be the same ones that Sherry and John have over at YoungHouseLove.com (although they were much more adventurous than I am and ended up painting it green). The other is located in our office/guest room, which for now is nice, but a much less inspired space.

The coffee table is the LACK coffee table from IKEA, which was about $20-$25 new. I got that because we have matching LACK side tables in the bedroom, and I liked the both the style and the potential to use them in the same room.

Curtains are from the Christmas Tree Shop (an amazing line of stores that is unfortunately only found in the Northeast). I wanted blue-grey silk curtains with a nice sheen, but could not talk myself into spending a ton on real silk. So instead I found them in faux silk at Christmas Tree Shop in Connecticut, and put them in my suitcase on my way back to Arizona! At about $15/two panels, they are much, much more affordable.

We also put the curtains in our dining room. (adjoins the living room at the point from where the pictures were taken) We have a wall with an ugly wood veneer built in cabinet, and cannot remove it since we are renting. Since I couldn't stand to look at it every single day, I had the idea to hang curtains on either side of the stainless steel shelves and cover the cabinet, while still allowing access to drawers. The other side of the metal shelving is where we store things like brooms and mop buckets, since we don't have room anywhere else in the apartment.

In this picture, the table is from Craigslist, while the metal shelves are from IKEA (about $80 for the set, but very durable - and it was the one piece of furniture my fiance really wanted in the apartment). The table cost $50 for a table and four chairs. I loved the lines on the back of the chairs, and so I'm hoping to make time in the next year to stain or paint it a darker wood color.

So there you have it. For less than $400 we added furniture and fabric to our living/dining room area and created a comfortable, inviting space. I must say, I'm addicted to Craigslist! (we got our new mattress and desk from Craigslist as well)

Side note: sorry about the poor picture quality and the weird lighting. I was using an unfamiliar camera but wanted to get the pictures taken!

Tasty Tuesday #5: Non-fried Eggplant Parmigiana

Eggplant Parmigiana:

1 eggplant, sliced 1/4-1/2 inch thick (I like to do it in strips along the length of the eggplant because it fits better in the baking pan) ($.88)

1 cup breadcrumbs + 1/4 cup parmesan cheese ($1.50)

2 eggs ($.50)

1/4 cup milk ($.25)

1 jar tomato sauce ($3.00)

1/2 cup shredded mozzerella ($1.00)

1/4 cup grated parmesan ($.50)

1 lb of spaghetti ($.99)

Directions:

Preheat the oven to 350. Cook 1lb of pasta (we used spaghetti).

Combine milk and egg in one bowl, breadcrumbs and parmesan in another bowl.

Coat the eggplant slices in the egg and milk mixture, then in the breadcrumbs.

Put the eggplant on a baking sheet covered in aluminum foil and non-stick spray.

Bake for 5 minutes on one side, and 5 minutes on the other.

Once they're all cooked, lay them layer them a glass baking dish, alternating with tomato sauce and cheese.

Cover with tomato sauce, sprinkle extra cheeses over top, and bake about 10 minutes.

Serve on top of pasta!

For $8.50, you've got enough food to feed at least four people (unless your fiance is as hungry as mine is - then it ends up being one dinner for us, plus leftover lunch for me). That's much better than paying an arm and a leg for a restaurant serving! If you crave the deliciousness that normally comes from a restaurant, try grating fresh mozzerella and parmesan cheese. It makes a huuuge difference, but unfortunately they don't come cheap.

Monday Money Saver #5: Starbucks Banana Walnut Bread

This week's Money Saver idea will be home-made Banana Walnut Bread. This recipe comes from one of the little cards they had sitting next to the register.

Ingredients:

2 cups flour

1 tsp baking soda

1/4 teaspoon salt

1 1/8 cup sugar

1/2 cup vegetable oil

1 egg

2 teaspoons buttermilk (to make buttermilk, add a splash of vinegar to the 2 tsp regular milk)

1/2 teaspoon vanilla

3 ripe bananas (mashed)

1/2 cup plus 1/3 cup chopped walnuts

Directions:

Pre-heat the oven to 325 degrees. Grease a 9x5x3 loaf pan and dust with flour.

Blend together the flour, baking soda and salt and set aside.

Mix together the eff, sugar, and vegetable oil until combined. Add the flour mixture and when blended, add the buttermilk, vanilla, and mashed bananas. Mix until combined. Fold in 1/2 cup chopped wanuts and pour batter into prepared loaf pan. Top batter with remaining 1/3 cup chopped walnuts. Bake for 45-60 minutes, until a toothpick uinserted in the center comes out clean. Cool for 10 minutes on a wire rack before removing from the pan.

I don't have the nutritional data for this, but generally when I get the banana nut bread it's because I want something tasty for breakfast, not because I know it's the best food for me.

Ingredients:

2 cups flour

1 tsp baking soda

1/4 teaspoon salt

1 1/8 cup sugar

1/2 cup vegetable oil

1 egg

2 teaspoons buttermilk (to make buttermilk, add a splash of vinegar to the 2 tsp regular milk)

1/2 teaspoon vanilla

3 ripe bananas (mashed)

1/2 cup plus 1/3 cup chopped walnuts

Directions:

Pre-heat the oven to 325 degrees. Grease a 9x5x3 loaf pan and dust with flour.

Blend together the flour, baking soda and salt and set aside.

Mix together the eff, sugar, and vegetable oil until combined. Add the flour mixture and when blended, add the buttermilk, vanilla, and mashed bananas. Mix until combined. Fold in 1/2 cup chopped wanuts and pour batter into prepared loaf pan. Top batter with remaining 1/3 cup chopped walnuts. Bake for 45-60 minutes, until a toothpick uinserted in the center comes out clean. Cool for 10 minutes on a wire rack before removing from the pan.

I don't have the nutritional data for this, but generally when I get the banana nut bread it's because I want something tasty for breakfast, not because I know it's the best food for me.

Taking Stock of the Past Year

This October marks the one year anniversary of my full time employment at my current job. This is my first full time permanent job, so when I started, I knew I had to buckle down and start getting serious with my paycheck.

Now that I've been getting those biweekly checks for a year, I figured it's about time to take stock of where all my money went. When I did take a look at where my money went, I was pleasantly surprised.

When you look at your past year, how do you feel you've done? Has the economy wrecked your well-laid plans, or have you been frugal and kept up your debt payments/savings? What are your goals for the next year?

Cash Buffer / Emergency Fund

Over the course of a year, I have been making regular contributions to a high interest checking account that serves as my cash buffer and emergency fund. Currently I have a few thousand dollars in this account. I would have had more, but when we moved to our new apartment, we used some of it to aid our cash flow (one security deposit came due before the other was returned to us). This is not a step I plan to repeat, but at the time it was the best option.

The peace of mind that comes along with having this cash buffer is incredible. My fiance changed jobs in the past year, from a full time but exhausting and unfulfilling job, to several part time jobs that are much more flexible and enjoyable. Despite the uncertainty of unemployment with the current recession, we were able to continue paying down debt and saving money without tapping into our emergency fund. But just knowing it was there if we needed it made the stress of the situation much, much less. I think many couples' money fights could be avoided if they can create similar financial priorities. We did cut back on going out to eat and our 'fun fund', because to us, saving money and reducing debt is much more important than splurging on restaurants and travel.

Paying Down Debt

This is one area that my fiance and I both know is crucial. We both have student loans from college, and we make regular monthly payments in excess of the minimum payment amount. Even though I am still in school, so my loans are technically in deferment (I don't have to start paying until I am no longer a full time student), I am paying them monthly anyway.

This pre-payment serves two purposes. First, it helps to decrease the amount of interest I will be charged over the life of the loan by decreasing the balance. My rates right now are currently very low (between 3.75% and 6.76%), but when I took out the loans the rates were very high (8-9%). Since a large amount of interest accrued at the higher rates, my payments go toward reducing this accumulated interest. Once I graduate, the interest will be added to the principal and will earn interest on top of interest. This is something I want to avoid as much as possible.

The second purpose of paying my loans before I absolutely have to is to prevent myself from getting used to having that extra spending money. Lets say for example, I pay $800 per month on my loans. If I weren't putting this toward loans, I could be living a much different lifestyle than I am now - fancy restaurants, travel, shopping, etc. But since I started putting this money toward loans as soon as I started getting a paycheck, I don't miss it. It would be much harder to change from that high-flying lifestyle and cut back to afford debt payments after graduation.

Retirement Savings

This is the area where I am most proud of how far I've come. This time last year, I knew absolutely nothing about saving for retirement. I had no idea how much people had to save to retire 'comfortably'. Nobody my age that I knew was saving - most were still looking for jobs. I did tons and tons of research online, and decided it would be dumb of me to not take advantage of the tax benefits provided for retirement savings.

Since my company was in the middle of a merger, and the 401k plan was not yet set up, I opened a Roth IRA for myself and started contributing. Once my company offered a 401k, I set up a Roth 401k with them (with a regular 401k for the employer's 3% safe harbor contribution) and started contributing 10% of my income. This 10% comes out of my paycheck before it even reaches my bank account - so I never miss it. I still contribute to my Roth IRA. Since any gains made in these accounts will never be taxed, starting early is critical.

Goals for the Next Year

Here's roughly what I accomplished in the last 12 months:

$10,000 in debt payments

$6,000 in retirement savings

$3,000 in cash buffer/emergency fund

Here's what I want to accomplish in the next 12 months:

-max out my Roth IRA ($5,000 per year)

-continue contributing 10% (plus 3% employer safe harbor) to 401k

-reach 3 months expenses (including minimum debt payments) in the emergency fund (another $5k to go)

-pay down $15,000 in debt

Now that I've been getting those biweekly checks for a year, I figured it's about time to take stock of where all my money went. When I did take a look at where my money went, I was pleasantly surprised.

When you look at your past year, how do you feel you've done? Has the economy wrecked your well-laid plans, or have you been frugal and kept up your debt payments/savings? What are your goals for the next year?

Cash Buffer / Emergency Fund

Over the course of a year, I have been making regular contributions to a high interest checking account that serves as my cash buffer and emergency fund. Currently I have a few thousand dollars in this account. I would have had more, but when we moved to our new apartment, we used some of it to aid our cash flow (one security deposit came due before the other was returned to us). This is not a step I plan to repeat, but at the time it was the best option.

The peace of mind that comes along with having this cash buffer is incredible. My fiance changed jobs in the past year, from a full time but exhausting and unfulfilling job, to several part time jobs that are much more flexible and enjoyable. Despite the uncertainty of unemployment with the current recession, we were able to continue paying down debt and saving money without tapping into our emergency fund. But just knowing it was there if we needed it made the stress of the situation much, much less. I think many couples' money fights could be avoided if they can create similar financial priorities. We did cut back on going out to eat and our 'fun fund', because to us, saving money and reducing debt is much more important than splurging on restaurants and travel.

Paying Down Debt

This is one area that my fiance and I both know is crucial. We both have student loans from college, and we make regular monthly payments in excess of the minimum payment amount. Even though I am still in school, so my loans are technically in deferment (I don't have to start paying until I am no longer a full time student), I am paying them monthly anyway.

This pre-payment serves two purposes. First, it helps to decrease the amount of interest I will be charged over the life of the loan by decreasing the balance. My rates right now are currently very low (between 3.75% and 6.76%), but when I took out the loans the rates were very high (8-9%). Since a large amount of interest accrued at the higher rates, my payments go toward reducing this accumulated interest. Once I graduate, the interest will be added to the principal and will earn interest on top of interest. This is something I want to avoid as much as possible.

The second purpose of paying my loans before I absolutely have to is to prevent myself from getting used to having that extra spending money. Lets say for example, I pay $800 per month on my loans. If I weren't putting this toward loans, I could be living a much different lifestyle than I am now - fancy restaurants, travel, shopping, etc. But since I started putting this money toward loans as soon as I started getting a paycheck, I don't miss it. It would be much harder to change from that high-flying lifestyle and cut back to afford debt payments after graduation.

Retirement Savings

This is the area where I am most proud of how far I've come. This time last year, I knew absolutely nothing about saving for retirement. I had no idea how much people had to save to retire 'comfortably'. Nobody my age that I knew was saving - most were still looking for jobs. I did tons and tons of research online, and decided it would be dumb of me to not take advantage of the tax benefits provided for retirement savings.

Since my company was in the middle of a merger, and the 401k plan was not yet set up, I opened a Roth IRA for myself and started contributing. Once my company offered a 401k, I set up a Roth 401k with them (with a regular 401k for the employer's 3% safe harbor contribution) and started contributing 10% of my income. This 10% comes out of my paycheck before it even reaches my bank account - so I never miss it. I still contribute to my Roth IRA. Since any gains made in these accounts will never be taxed, starting early is critical.

Goals for the Next Year

Here's roughly what I accomplished in the last 12 months:

$10,000 in debt payments

$6,000 in retirement savings

$3,000 in cash buffer/emergency fund

Here's what I want to accomplish in the next 12 months:

-max out my Roth IRA ($5,000 per year)

-continue contributing 10% (plus 3% employer safe harbor) to 401k

-reach 3 months expenses (including minimum debt payments) in the emergency fund (another $5k to go)

-pay down $15,000 in debt

Wednesday Websites #4: Retirement Accounts

Since this is National Save for Retirement Week, today's websites will feature online companies that allow you to create and maintain retirement savings accounts.

Before I launch into a list of links, I'll give a quick background of the different types of accounts. I'll go into each in more detail later this week, but for now, lets say there are two major types of retirement accounts.

The first is the 401k. This is a tax advantaged account that is generally an 'employer-sponsored' plan. That means, when you leave one job for another, you have to transfer your 401k account to your new employer. Many employers also offer matching contributions, say for 3% of salary. Employer contributions are free money - make sure you are taking advantage of it!

The second type of account is the IRA, or Individual Retirement Account. Like it's name implies, this account is tied to you, not your employer. You can change jobs every week if you'd like, but you don't have to change your account information for an IRA. You do not get employer matching for this type of account.

There are limits as to how much money you can put in each account during the year, since they are "tax advantaged" accounts. That means that there are tax benefits associated with saving for retirement.

If you choose the 'traditional' IRA or 401k, you put money in pre-tax, and are only taxed when you make withdrawals in retirement. This type of account is good if you think your tax bracket is higher now than it will be when you retire. It also serves to decrease your current taxable income, so you will pay fewer taxes in the present.

If you choose the "Roth" IRA or 401k, your money is put in after taxes have already been taken out, but you never have to pay tax on the gains that investment makes. So if you manage to turn $10,000 into $100,000 by the time you retire, you will have been taxed on the original $10,000 at your current tax rate, but you will not be taxed on the $90,000 your money earned. This type of account is best if you think your tax rate now is lower than what it will be when you retire. So if you are starting out at an entry level job in one of the lower tax brackets, this may be the best account for you currently.

You can also have both. I currently do - I put money into both a Roth IRA and Roth 401k, but my employer's contribution gets directed to a Traditional 401k.

Now that you get the basic idea of what types of accounts there are, here is a listing of websites that allow you to create and fund your own account.

Etrade

ING Direct

Fidelity

Bank of America

Scottrade

Note: You should check out the list of potential fees before opening any account. Some of these sites will charge an annual fee, but not charge for trades, while others will charge for trading but not have an annual fee. You need to determine how you will most likely handle your money, and pick the one that suits your personal investment style.

Before I launch into a list of links, I'll give a quick background of the different types of accounts. I'll go into each in more detail later this week, but for now, lets say there are two major types of retirement accounts.

The first is the 401k. This is a tax advantaged account that is generally an 'employer-sponsored' plan. That means, when you leave one job for another, you have to transfer your 401k account to your new employer. Many employers also offer matching contributions, say for 3% of salary. Employer contributions are free money - make sure you are taking advantage of it!

The second type of account is the IRA, or Individual Retirement Account. Like it's name implies, this account is tied to you, not your employer. You can change jobs every week if you'd like, but you don't have to change your account information for an IRA. You do not get employer matching for this type of account.

There are limits as to how much money you can put in each account during the year, since they are "tax advantaged" accounts. That means that there are tax benefits associated with saving for retirement.

If you choose the 'traditional' IRA or 401k, you put money in pre-tax, and are only taxed when you make withdrawals in retirement. This type of account is good if you think your tax bracket is higher now than it will be when you retire. It also serves to decrease your current taxable income, so you will pay fewer taxes in the present.

If you choose the "Roth" IRA or 401k, your money is put in after taxes have already been taken out, but you never have to pay tax on the gains that investment makes. So if you manage to turn $10,000 into $100,000 by the time you retire, you will have been taxed on the original $10,000 at your current tax rate, but you will not be taxed on the $90,000 your money earned. This type of account is best if you think your tax rate now is lower than what it will be when you retire. So if you are starting out at an entry level job in one of the lower tax brackets, this may be the best account for you currently.

You can also have both. I currently do - I put money into both a Roth IRA and Roth 401k, but my employer's contribution gets directed to a Traditional 401k.

Now that you get the basic idea of what types of accounts there are, here is a listing of websites that allow you to create and fund your own account.

Etrade

ING Direct

Fidelity

Bank of America

Scottrade

Note: You should check out the list of potential fees before opening any account. Some of these sites will charge an annual fee, but not charge for trades, while others will charge for trading but not have an annual fee. You need to determine how you will most likely handle your money, and pick the one that suits your personal investment style.

Tasty Tuesday #4: Lemon Poppy Seed Muffins

Lemon Poppy Seed Muffins are one of my all time favorite kinds of muffins. But if you get them at your local bakery/coffee shop, they're likely to charge you upwards of $3 for one single muffin! So I find the best way to get delicious muffins, save money, and know exactly what is in my food (I like avoiding preservatives and ingredients that are impossible to pronounce as much as possible), is to make my own muffins. These come out moist, delicious, and refreshingly lemony, without being overbearing.

Lemon Poppy Seed Muffins are one of my all time favorite kinds of muffins. But if you get them at your local bakery/coffee shop, they're likely to charge you upwards of $3 for one single muffin! So I find the best way to get delicious muffins, save money, and know exactly what is in my food (I like avoiding preservatives and ingredients that are impossible to pronounce as much as possible), is to make my own muffins. These come out moist, delicious, and refreshingly lemony, without being overbearing. Here's the recipe!

Ingredients:

3 cups unbleached all purpose flour ($0.50)

1 cup honey ($0.50)

3 tbsp poppy seeds ($0.25)

1 tbsp grated lemon peel ($0.75)

1 tsp baking soda ($0.05

2 tsp baking powder ($0.05)

1/2 tsp salt (negl. $)

16 oz plain low-fat yogurt ($1.00)

1/2 cup fresh lemon juice ($0.75)

1/4 cup applesauce ($0.10)

2 eggs ($0.25)

1 1/2 tsp vanilla ($0.10)

Preparation:

Preheat oven to 400. Grease 12 large muffin cups (or smaller muffin cups and a bread pan, which is what is pictured above).

Combine flour, poppy seeds, lemon peel, baking powder, baking soda, and salt in large bowl. Combine all other ingredients in small bowl until well blended. Stir into flour mixture just until moistened. Spoon into muffin cups, filling 2/3 full.

Bake 25-30 minutes (about 15 minutes if you are making small ones - don't make the same mistake I did and burn the edges by cooking them too long!) (25-30 is also good if you make it in two small bread pans - lemon poppyseed loaf anyone?). Cool until ready to serve.

Cost:

Total cost - about $5.20

Cost per serving - about $0.65

Nutrition Facts:

click here

Monday Money Saver #4: OpenOffice.org

Chance are if you are reading this post, you own a computer. That same computer also probably has a suite of programs used for editing text, spreadsheets, presentations, and things like that. Given that somewhere between 80 and 95% of computers run Microsoft Office, you probably have Microsoft Word, Excel, and Powerpoint. Most new computers come with these programs already installed, so the price has been worked into the purchase price. But according to their website, this suite of programs runs approximately between $150 (student version) and $680 (business version), depending on which programs you include in your purchase. The typical home package (includes Microsoft Outlook) runs about $300.

$300??? That seems like an exorbitant amount of money that could be better spent upgrading the physical capabilities of the computer, or just saved.

Never fear - you can save that $300 by downloading Open Office. Open Office is an "open source" software, which means that any computer geek can edit and improve the software package. Microsoft Office is proprietary, so only Microsoft can change it legally.

The programs included in the Open Office suite include your basic word, spreadsheet, and presentation editing software. But it also includes a graphics editing program and a database program, which aren't even included in the cheapest Microsoft download.

Even better, the Open Office suite of programs allows you to select the file type as you save a file. That means when you save the word file you just created, you can save it as *.doc, and then it can be opened in Microsoft Word. The files are almost completely interchangeable with Microsoft Office files, with the sole exception being some of the newer features of Microsoft Office 2007. If you know anything about Office versions, saving a document in Open Office is like saving it in Microsoft Office 2003.

If you don't want to spend hundreds of dollars for software, or you lost your Microsoft installation disk and don't want to buy it again, try Open Office. I've used it in the past, and it is very user friendly. Their website even has a support forum in case you really have trouble.

$300??? That seems like an exorbitant amount of money that could be better spent upgrading the physical capabilities of the computer, or just saved.

Never fear - you can save that $300 by downloading Open Office. Open Office is an "open source" software, which means that any computer geek can edit and improve the software package. Microsoft Office is proprietary, so only Microsoft can change it legally.

The programs included in the Open Office suite include your basic word, spreadsheet, and presentation editing software. But it also includes a graphics editing program and a database program, which aren't even included in the cheapest Microsoft download.

Even better, the Open Office suite of programs allows you to select the file type as you save a file. That means when you save the word file you just created, you can save it as *.doc, and then it can be opened in Microsoft Word. The files are almost completely interchangeable with Microsoft Office files, with the sole exception being some of the newer features of Microsoft Office 2007. If you know anything about Office versions, saving a document in Open Office is like saving it in Microsoft Office 2003.

If you don't want to spend hundreds of dollars for software, or you lost your Microsoft installation disk and don't want to buy it again, try Open Office. I've used it in the past, and it is very user friendly. Their website even has a support forum in case you really have trouble.

National Save for Retirement Week

In honor of National Save for Retirement week, we will be having a week of posts dedicated to saving for retirement. Check back next week for posts about retirement planning, tax advantaged accounts, and other helpful information. In the meantime, take the poll about your retirement planning!

Congress established National Save for Retirement Week to increase awareness of the need to save for retirement.

In 2009, the House of Representatives and the U.S. Senate unanimously approved resolutions designating Oct. 18-24 as National Save for Retirement Week. The resolutions seek to increase personal financial literacy and raise public awareness of the retirement-savings vehicles available to all workers, including public- and private-sector employees, employees of tax-exempt organizations, and self-employed individuals.Research shows that more than half of all workers in the United States, 53 percent, have less than $25,000 in total savings and investments, excluding their home and defined benefit plans. With longer life expectancies and rising costs, especially for health care, it is critical that Americans understand the importance of saving for their future - now.

^Above information from http://www.retirementweek.org/xp/plans/retirementweek/

Blog Action Day

I have my own opinions, but since I know everyone is entrenched in their own beliefs, I'll refrain from preaching or lecturing. Instead, I'd like to highlight one critical problem that faces much of the world, and will be acutely aggravated by climate change (human cause or natural).

Water Resources

Much of the developing world lacks access to clean water sources. Many illnesses in third world countries are caused by inadequate water treatment and contamination from waste and trash. Simple bacteria can cause the deaths of an entire village, which is something we take for granted in the United States. Water treatment facilities can be fairly inexpensive, but most rural third world communities lack the technical knowledge or financial resources to complete these projects. As climate change shifts weather patterns, water will become more scarce in already arid regions, and flooding will occur in already rainy areas. These weather changes will exacerbate the problem of access to clean drinking water.

The Water Project is dedicated to providing clean drinking water for impoverished countries. Please help.

Wednesday Website #3: Gift Cards at a Discount

On Monday we featured a way to save on your digital music habits. This week's Wednesday Website is a great way to save money at stores you already know you're going to shop at, or to save money on gifts for birthdays or holidays.The following websites feature gift cards at a discount - 10%, 15%, or more.

Plastic Jungle: Probably the most popular of the gift card recycling websites, Plastic Jungle has a cute, user friendly interface and a slew of merchants to choose from. You can find almost any store you need - Home Depot, Lowe's, Macy's, Sears, Best Buy, Victoria's Secret, Old Navy, TJ Maxx, JC Penney, you name it. They also offer some pretty awesome discounts. As I write this, they are offering a $25 Godiva gift card for only $17.50. That's a great way to save some serious cash on your Christmas shopping! Even better, if you are feeling philanthropic, you can choose to donate 100% of the amount on your card to a classroom in need.

GiftCards.com: This website is a little less fashionable/user-friendly, but it does have spots where it outshines Plastic Jungle. They too have discounted gift cards for common merchants, though the selection is a little more limited. On the up side, they have an option to create customizable VISA gift cards. You can choose your amount, upload a photo, and have it sent to the person in a personalized card. This is great if you can't figure out what someone wants as a gift, but want a little more security than giving out cash.

Tasty Tuesday #3: Homemade Chai Tea

Boil a large pot of water on the stove, like you were going to make a couple pounds of pasta, but without the salt/oil.

When it's boiling, add 6 black tea bags and steep for maybe 5 minutes. Also add the following:

2 tbsp cinnamon

1 tsp fennel (crushed - use a mortar/pestle or a wooden spoon in a bowl)

1 tbsp nutmeg

1 tbsp vanilla extract

1 tbsp crushed cloves

1/2 tsp fresh ground black pepper

1/4 cup honey (stir well so it doesn't sit on the bottom)

After steeping the black tea bags sufficiently (the water will turn a dark brownish/black), remove the tea bags, but let the other spices steep for another 15 minutes or so.

If you want to enjoy it hot, ladle out a mug or two while the spices are steeping. Heat some milk in the microwave (or the stove if you're careful not to burn it) and mix with about 1 part of each. You can reheat the tea at a later time in the microwave if it cools off too much.

If you want it iced - let it steep for maybe half an hour. It should be brewed stronger, since the ice will dilute the tea. Once it is cool to the touch, pour it into a pitcher while straining out the spices with a paper towel spread over a metal colander (to catch the fine spices). Then, add cold milk for a refreshing, slightly caffeinated, spicy treat!

Given the fact that you can buy black tea bags in bulk for around 100 bags for $2.00, the spices are fairly inexpensiv, and milk is generally inexpensive as well, a gallon of chai tea should cost you no more than a buck or two. That's much, much better than going to a fancy coffee store and spending $4 per cup. If you really want creamy chai, try adding a dash of half and half to get that nice smooth mouth-feel, or use whole milk (we normally buy 1% or 2%, so the extra fat makes a big difference).

Monday Money Saver #3: Free Music

I know it's pretty easy to hear a song you like, and click a couple clicks, pay the $0.99, and download it to your computer. But that adds up really fast. A few songs a week and you're at a couple hundred dollars per year!

But there is a better way - as long as you have an internet connection! The following websites are excellent places to listen to free music - legally.

1. Pandora - pandora.com

Pandora is a website that uses algorithms to identify similar songs or artists. For example, if you want to play a station full of classic rock, enter in a few artists like Led Zeppelin or the Beatles, and it will populate the station with similar songs and artists. If you want pop circa 2000, "seed" the station with Britney Spears, Christina Aguilera, Backstreet Boys, or 'N Sync. You can give a song a thumbs up if you want to hear more like it, or a thumbs down if you don't want it played on that station ever again.

I am pretty sure you can create an unlimited number of stations - at least I haven't hit the limit yet. You can create stations for different moods - I have a "spa" station that I like to listen to while doing yoga, a punk rock station I put on when I'm cleaning the apartment, or even a christmas station I like to play while baking cookies.

The only frustrating thing about Pandora is that you can't ask it to play a specific song. The song you like might show up on your station, but you can't control when it plays. Also, if you listen to more than 30 hours of music in a month, you have to pay a $0.99 fee to continue listening. Even with these little frustrations, Pandora is an awesome music playlist. To keep it free, they do run ads occasionally - but not much more frequently than one 15-20 second ad per half hour. I highly recommend Pandora to those people who want to hear new music in a specific genre, but don't want to test out songs by buying them from iTunes or Amazon.

2. Playlist.com - playlist.com

Playlist.com is the answer to Pandora's inability to play a song on demand. While Pandora is good for generating new music that is similar to music you already like, Playlist is good for listening to songs you already know you like. You can search for specific songs or artists, and then add them to your playlist. So if you want a playlist with every Spice Girl song possible, you can create that, and listen to it as many times as you want. Like Pandora, they play ads on the webpage, but they are minimally invasive. Playlist is great if you've got a song stuck in your head and need to listen to it before it drives you nuts.

Now neither of these websites will work unless you are connected to the internet. For that, you will still need to download your music from a place like Amazon or iTunes. But as long as you have an internet connection, these websites will help curb your purchasing habit, and you can share your stations/playlists with friends. The other great thing is that Pandora is available for many mobile phones - it works on my Blackberry and I'm sure it works on the iPhone as well. Playlist.com won't work on phones yet, until they support Flash.

In the meantime, check them out and let me know what you think!

But there is a better way - as long as you have an internet connection! The following websites are excellent places to listen to free music - legally.

1. Pandora - pandora.com

I am pretty sure you can create an unlimited number of stations - at least I haven't hit the limit yet. You can create stations for different moods - I have a "spa" station that I like to listen to while doing yoga, a punk rock station I put on when I'm cleaning the apartment, or even a christmas station I like to play while baking cookies.

The only frustrating thing about Pandora is that you can't ask it to play a specific song. The song you like might show up on your station, but you can't control when it plays. Also, if you listen to more than 30 hours of music in a month, you have to pay a $0.99 fee to continue listening. Even with these little frustrations, Pandora is an awesome music playlist. To keep it free, they do run ads occasionally - but not much more frequently than one 15-20 second ad per half hour. I highly recommend Pandora to those people who want to hear new music in a specific genre, but don't want to test out songs by buying them from iTunes or Amazon.

2. Playlist.com - playlist.com

Now neither of these websites will work unless you are connected to the internet. For that, you will still need to download your music from a place like Amazon or iTunes. But as long as you have an internet connection, these websites will help curb your purchasing habit, and you can share your stations/playlists with friends. The other great thing is that Pandora is available for many mobile phones - it works on my Blackberry and I'm sure it works on the iPhone as well. Playlist.com won't work on phones yet, until they support Flash.

In the meantime, check them out and let me know what you think!

Step 4: All About Automation

Sorry for the late post - I ran my first 5k this weekend and posting got pushed to the side. Check back for the next Monday Money Savers post later today!

Banks do whatever they can to make money, and they have no qualms about charging you $40 here or there for minor mistakes.

In Step 1, you listed all of your financial accounts. In Step 2, you checked this list against your credit report, and found any late payments you might have made. In Step 3, you came up with a budget or spending plan. Now, in Step 4, you will set up your accounts to function automatically so you don't waste money on fees and penalties.

It may seem like a minor step, but doing this can potentially save you hundreds of dollars over the course of a few years

If you use debit cards instead, and you overdraw your account one day, you can rack up $40 fees for each purchase you make. You may think you have enough money to buy the coffee in the morning, and then overdraft for a larger purchase in the afternoon - but banks can and do reorder your purchases to make you go over the limit faster, so you can potentially rack up fees on each purchase. That $4 cup of coffee just cost you $44.

The easiest way to avoid these problems is to automate your accounts. To start with your debit accounts, check with your bank to see how they handle overdrafts. Some banks and credit unions will not charge you to transfer money from your savings to checking automatically to cover your purchases. Others will. Other banks use your debit account as a sort of credit account - charging you fees and interest until you pay back what you have 'borrowed'. The easiest way to avoid these fees is to do some research and find a bank that won't nickle and dime you. It may take some time up front, but it will save you time and headaches down the line.

For credit cards, utilities accounts, and other debts, many of the fees and penalties will come from late payments, rather than 'overdrafts'. The easiest way to avoid these is to automate your payments, so you never have to worry about missing the due date. I like to use the direct debit method of payment, set up through online banking, that allows monthly payments to be automatically deducted from a checking account. In my checking account, I always make sure to have at least the minimum amount required to meet my minimum payments.

Let's say I have 2 credit cards, a cell phone bill, and an electricity bill due every month (for simplicity's sake). If each credit card has a minimum payment of $15, and each bill costs approximately $50 per month, I need to make sure my account has a minimum of $130 at all times. This amount should be an emergency amount, and should be replenished if you do end up needing to use it. By keeping this buffer, you won't have to worry about overdrafts or late payments, and you'll save both time and money.

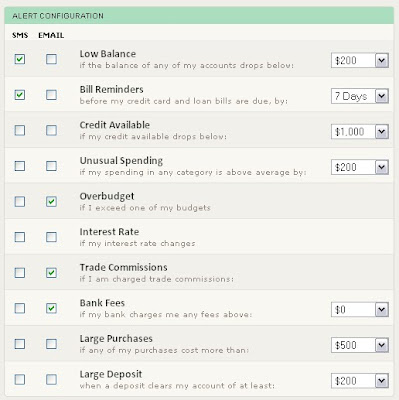

The other thing I swear by is the "alerts" feature at mint.com. Like I mentioned in my previous post about Mint, they have a feature that allows you to set alerts for different events. If you go over your budget in one area, it can send you an alert. If you have a credit card payment due, you can set an alert. Use these automated features to your advantage. Set it up to remind yourself 2 weeks before your bill is due, so you have time to transfer money if you need to.

Banks do whatever they can to make money, and they have no qualms about charging you $40 here or there for minor mistakes.

In Step 1, you listed all of your financial accounts. In Step 2, you checked this list against your credit report, and found any late payments you might have made. In Step 3, you came up with a budget or spending plan. Now, in Step 4, you will set up your accounts to function automatically so you don't waste money on fees and penalties.

It may seem like a minor step, but doing this can potentially save you hundreds of dollars over the course of a few years

If you use debit cards instead, and you overdraw your account one day, you can rack up $40 fees for each purchase you make. You may think you have enough money to buy the coffee in the morning, and then overdraft for a larger purchase in the afternoon - but banks can and do reorder your purchases to make you go over the limit faster, so you can potentially rack up fees on each purchase. That $4 cup of coffee just cost you $44.

The easiest way to avoid these problems is to automate your accounts. To start with your debit accounts, check with your bank to see how they handle overdrafts. Some banks and credit unions will not charge you to transfer money from your savings to checking automatically to cover your purchases. Others will. Other banks use your debit account as a sort of credit account - charging you fees and interest until you pay back what you have 'borrowed'. The easiest way to avoid these fees is to do some research and find a bank that won't nickle and dime you. It may take some time up front, but it will save you time and headaches down the line.

For credit cards, utilities accounts, and other debts, many of the fees and penalties will come from late payments, rather than 'overdrafts'. The easiest way to avoid these is to automate your payments, so you never have to worry about missing the due date. I like to use the direct debit method of payment, set up through online banking, that allows monthly payments to be automatically deducted from a checking account. In my checking account, I always make sure to have at least the minimum amount required to meet my minimum payments.

Let's say I have 2 credit cards, a cell phone bill, and an electricity bill due every month (for simplicity's sake). If each credit card has a minimum payment of $15, and each bill costs approximately $50 per month, I need to make sure my account has a minimum of $130 at all times. This amount should be an emergency amount, and should be replenished if you do end up needing to use it. By keeping this buffer, you won't have to worry about overdrafts or late payments, and you'll save both time and money.

The other thing I swear by is the "alerts" feature at mint.com. Like I mentioned in my previous post about Mint, they have a feature that allows you to set alerts for different events. If you go over your budget in one area, it can send you an alert. If you have a credit card payment due, you can set an alert. Use these automated features to your advantage. Set it up to remind yourself 2 weeks before your bill is due, so you have time to transfer money if you need to.

Friday Freebie #2: Oregon Chai

Update: Sorry, it looks like they've run out of supplies! I'll keep my eyes open for new freebies!

Yes, it seems I'm on a free caffeinated beverage kick. I found this link for free samples of Oregon Chai and figured I'd pass it on! So head on over and get some for yourself!

Yes, it seems I'm on a free caffeinated beverage kick. I found this link for free samples of Oregon Chai and figured I'd pass it on! So head on over and get some for yourself!

October Wedding Update

Ok, ok.. I know this is supposed to be a blog about making the most of money, and generally a traditional wedding costs a lot. BUT, my parents want me to have a traditional wedding in a church, with a reception, and they are paying, so I can't say no (and honestly I'm excited!). Anyway, we are about 9 months out from the wedding right now, and some planning is done - but so much still needs to happen!

Here's where we stand on the to do list.

1: Ceremony Venue - check!

3: Wedding Dress - check! (but that's not me in the pic.. haha)

4: Bridesmaids Dresses - check!

5: Photographer - mailed the deposit today!

6: Grooms(men) attire - not yet, but it will look like this:

7: Save the Dates - not yet, but they're designed (they'll be magnets) and the guest list is almost finalized! (and the wedding website is up, which is blanked out below)

8: Flowers - not yet, I know I want Alstroemeria, but need to make more decisions about what arrangements will look like.

9: Invitations - not yet

10: DJ - not yet

11: Cake - not yet

12: Transportation - not yet

13: Rehearsal Dinner - not yet

14: Everything else - not yet!!!

So we still have a ways to go, but now that I've got the ceremony and reception venue, and the photographer, I feel a lot better! The rest of the stuff is less critical, since there are plenty of DJs, bakers, and restaurants in the area. Planning from 2500 miles away is difficult, but so far things are running pretty smoothly! (knock on wood!)

Here's where we stand on the to do list.

1: Ceremony Venue - check!

2: Reception Venue - check!

5: Photographer - mailed the deposit today!

{kind=link}

10: DJ - not yet

11: Cake - not yet

12: Transportation - not yet

13: Rehearsal Dinner - not yet

14: Everything else - not yet!!!

So we still have a ways to go, but now that I've got the ceremony and reception venue, and the photographer, I feel a lot better! The rest of the stuff is less critical, since there are plenty of DJs, bakers, and restaurants in the area. Planning from 2500 miles away is difficult, but so far things are running pretty smoothly! (knock on wood!)

Michael Jackson's Credit Score

The other day I wrote about credit scores and mentioned that even rich people can have low scores. Right on cue, Jeanne Kelly over at Huffington Post wrote about Michael Jackson's poor credit score - averaging 564! Considering a score under 620 indicates 'subprime' borrowers, even the King of Pop can run into financial trouble. In this case, don't be like Mike!

The other day I wrote about credit scores and mentioned that even rich people can have low scores. Right on cue, Jeanne Kelly over at Huffington Post wrote about Michael Jackson's poor credit score - averaging 564! Considering a score under 620 indicates 'subprime' borrowers, even the King of Pop can run into financial trouble. In this case, don't be like Mike!

Wednesday Website #2: Mint.com

Here it is: the number one website for keeping track of your money - and best of all, it's free!

I discovered Mint about a year ago, and it has made my life so much easier. The basic premise of the site is aggregation of your accounts. You enter your online login information for your banking, loans, or other financial accounts, and then Mint combines them all into one easy to use tool. This is not a paid endorsement, I didn't get any freebies (other than the use of their site, which is always free) - it just has worked wonders for me.

There are a few areas where Mint is very very helpful. I find numbers 4 and 5 below to be the most helpful.

1: Categorizing your spending.

Mint automatically categorizes all transactions in your transaction history into different categories. For example, a credit card charge at (insert grocery store name here) will automatically be categorized as groceries, or food and dining. A trip to Shell will be categorized as gas. When these are categorized, you can view your expenses as part of a whole - do you spend 1% or 10% of your money on gas?

2: Tracking your spending over time.

Mint also allows you to compare your spending from month to month or year to year. You can see where your expenses have changed.

3: Compare your spending to others.

By anonymizing your data and others on the site, you can compare your spending habits to other people in your city, region, or nation-wide. If you see that you're spending $500 more per year on auto insurance than the average person, you can take action to try and find cheaper rates.

4: Simple, easy budgeting.

The best feature on Mint is the budget tool. Remember that plan you came up with in Step 3? Well here is where you make it nearly automatic and incredibly easy. Enter your budgeted amounts into Mint's categories (groceries, gas, insurance, etc) and then relax.

That categorizing aspect I mentioned above? It comes into play here. When you buy groceries, it will automatically deduct that amount from your budgeted amount. You can see how much you have left, in relation to how much time is left in the month. You also have the option to roll over budgets from month to month, so if you spend $400 out of $500 one month, you get an extra $100 to spend the next. Or, conversely, if you overspend one month, it can deduct it from the next month's budget.

5: Alerts

The last really helpful feature Mint offers is the ability to set alerts. You can have these alerts sent in an email or as a text message. You can set alerts to tell you when you have a low balance, when you exceed your budget, when bills are do, or a whole host of other important things. That way, if you exceed your 'shopping' budget for the month, you can get an email to remind yourself not to spend anymore until the next month.

I discovered Mint about a year ago, and it has made my life so much easier. The basic premise of the site is aggregation of your accounts. You enter your online login information for your banking, loans, or other financial accounts, and then Mint combines them all into one easy to use tool. This is not a paid endorsement, I didn't get any freebies (other than the use of their site, which is always free) - it just has worked wonders for me.

There are a few areas where Mint is very very helpful. I find numbers 4 and 5 below to be the most helpful.

1: Categorizing your spending.

Mint automatically categorizes all transactions in your transaction history into different categories. For example, a credit card charge at (insert grocery store name here) will automatically be categorized as groceries, or food and dining. A trip to Shell will be categorized as gas. When these are categorized, you can view your expenses as part of a whole - do you spend 1% or 10% of your money on gas?

Mint also allows you to compare your spending from month to month or year to year. You can see where your expenses have changed.

By anonymizing your data and others on the site, you can compare your spending habits to other people in your city, region, or nation-wide. If you see that you're spending $500 more per year on auto insurance than the average person, you can take action to try and find cheaper rates.

4: Simple, easy budgeting.

The best feature on Mint is the budget tool. Remember that plan you came up with in Step 3? Well here is where you make it nearly automatic and incredibly easy. Enter your budgeted amounts into Mint's categories (groceries, gas, insurance, etc) and then relax.

5: Alerts

The last really helpful feature Mint offers is the ability to set alerts. You can have these alerts sent in an email or as a text message. You can set alerts to tell you when you have a low balance, when you exceed your budget, when bills are do, or a whole host of other important things. That way, if you exceed your 'shopping' budget for the month, you can get an email to remind yourself not to spend anymore until the next month.

Tasty Tuesday # 2: Black Bean Tomato Quinoa Salad

With my crazy schedule - 40 hours of work per week, plus a full-time master's degree program, along with training for a 1/2 marathon and working as an alumnae adviser for my college sorority - I need to save as much time as possible. One easy way to do this is to cook lunches on weekends and take them to work throughout the week. - it's incredibly healthy and very very tasty. I got the recipe from epicurious, and have added my own tweaks to make it more simple and savory. Here's how:

With my crazy schedule - 40 hours of work per week, plus a full-time master's degree program, along with training for a 1/2 marathon and working as an alumnae adviser for my college sorority - I need to save as much time as possible. One easy way to do this is to cook lunches on weekends and take them to work throughout the week. - it's incredibly healthy and very very tasty. I got the recipe from epicurious, and have added my own tweaks to make it more simple and savory. Here's how:Black Bean Tomato Quinoa Salad:

2 teaspoons grated lime zest ($.10)

2 tablespoons fresh lime juice ($.60)

1 tablespoon olive oil ($.10)

1 teaspoon honey ($.10)

1 cup quinoa ($.50)

1 (14- to 15-ounce) can black beans, rinsed and drained ($.50)

4 medium roma tomatoes, diced ($1.00)

1/4 cup leeks, scallions or onions, chopped ($.75)

1/4 cup chopped fresh cilantro ($1.00)

1 medium avocado ($.55)

1 tsp cayenne pepper sauce ($.05)

salt and pepper to taste (negl)

Directions:

Rinse the quinoa until the water runs clear and flaky grains to not float to the surface. Cook the quinoa as you would rice (1 cup grain to 1 cup water), for about 15 minutes. Drain well. Mix the first 4 ingredients in a bowl. Add quinoa. Stir in tomatoes, leeks, cilantro, avocado, cayenne pepper sauce, and salt/pepper until well mixed. Serve hot or cool for a tasty treat!

Cost:

around $5.25 for 4 servings - one serving in a wrap works perfectly for lunch for me!

Nutrition Info:

Black Bean Tomato Quinoa Salad

{kind=link}

Check out the nutritional info - this salad scores major points for critical nutrients like fiber, vitamin C, and iron.

Monday Money Saver #2: DIY Popcorn

Growing up in the microwave era, most of us have been exposed to popcorn in either those little microwaveable bags, or at the movie theatre. But the cost of those snacks adds up very, very quickly. At $4-5 per box, and only a handful of microwave servings per box, you can go through a box in a week if you've got a big Netflix queue to watch.

But there is a better way! You can buy the kernels themselves (also at the grocery store) for a fraction of the cost of microwave popcorn. Popcorn kernels run about $2 for a bag that should last a few weeks. All you need to do it yourself is a pot with a lid, some oil, and whatever toppings you feel like adding. Best of all, you don't have to buy 5 different kinds of popcorn if you want to mix it up a little, you can just make it yourself each time. It takes a little bit more involvement than the microwaveable kind, and maybe another minute or two, but it makes a huge difference. Homemade popcorn is also a lot better for you, and for the workers in popcorn factories. The powdered butter they put in microwaveable popcorn can cause serious health problems, including bronchiolitis obliterans, or Popcorn Lung.

Directions:

1: Pour a few tablespoons of oil into the pot.

2: Throw in two or so kernels (not all of them at once!).

3: Heat the oil until those two kernels pop.

4: Pour in the rest of the popcorn (1/4-1/2 cup is enough for a couple people). Shake the pot (while keeping over the heat) so that the kernels pop evenly.

5: Let it pop!! Keep popping until you don't hear many more pops.

6: Pour into a bowl, and sprinkle your favorite toppings - then enjoy!

Here's a few ideas of popcorn toppings you can try:

- pour melted butter on popcorn, sprinkle with salt

- pour a tiny bit of melted butter on the popcorn, then sprinkle cinnamon and sugar

- pour a tiny bit of melted butter, then add some grated parmesan/romano cheese, or powdered cheddar

- pour a tiny bit of melted butter, then add a pinch of garlic powder and some dried chives

- pour a tiny bit of hot sauce, then add chili powder and a pinch of cinnamon

Another good option is to make 'dessert popcorn':

1: Spread popcorn out on a wax paper or foil -lined baking sheet.

2: Melt some chocolate chips, butterscotch chips, white chocolate chips, or other form of sugary goodness in a glass measuring cup in the microwave.

3: Drizzle over the popcorn.

4: Freeze it until the chocolate is hardened. Then enjoy!

Step 3: Building a Budget for Busy People

In Step 1, you created a list of every account you have - both assets and liabilities.

In Step 2, you checked your credit report to make sure everything was correct.

Now that you have a handle your current and past financial transactions, Step 3 involves creating a plan for future transactions. Having a plan is critical to getting your finances on track. There are thousands of cliche statements about having a plan - failing to plan is planning to fail, a man who does not plan long ahead will find trouble right at his door, a good plan today is better than a perfect plan tomorrow.

Ok so you get the point. Now, some people call their financial plan a budget, some people who don't like the word 'budget' call it a spending plan. Call it whatever you like - the important thing is that you make one!

Luckily, I have found one of the best (and easiest) ways to create this plan. Go to this website and download the spreadsheet by Michael Ham. Fill in as much information as you possibly can - income, debts, retirement goals, plans for buying things in the future, utilities, health insurance (if you are lucky enough to have it) - anything you can think of. If you think you will die without your "eating out" money, or going shopping, by all means add it in. The purpose of creating a budget is not to deny yourself the ability to spend money on things you enjoy. The purpose is to make sure that you can afford the things you want to do and aren't going into unnecessary debt to finance your lifestyle.

Don't forget to budget for emergency savings, either. Without this cash buffer, you are all too vulnerable to unforeseen problems and emergency expenses, which can make you all too dependent on credit cards, or worse, pay-day-loans. You need to have cash set aside in case your car breaks down, in case the air conditioning or heating breaks, or whatever else might happen.